Mortgage Rates Today: What Borrowers Should Know in a Volatile Housing Market

An up-to-date, in-depth look at mortgage rates and what’s driving today’s lending environment. Learn how borrowers can navigate rate shifts, compare lenders effectively, and secure the strongest mortgage option available now.

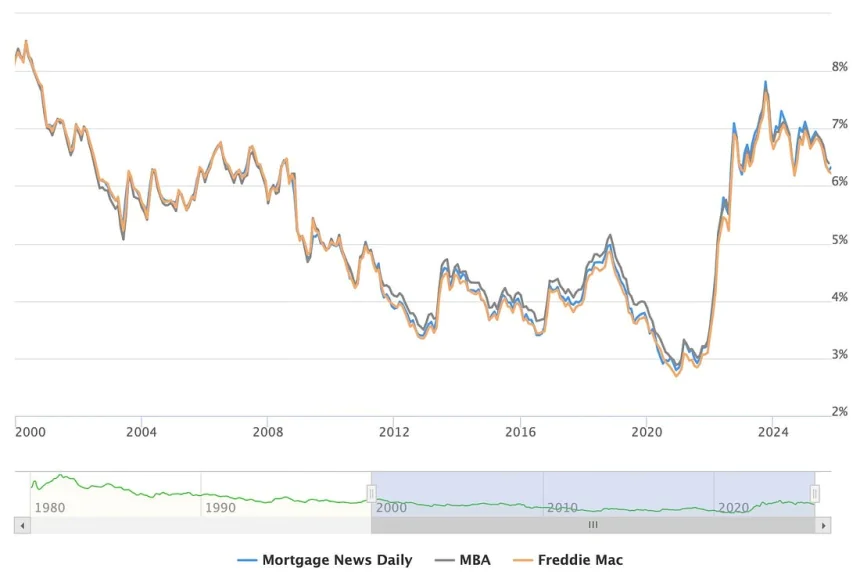

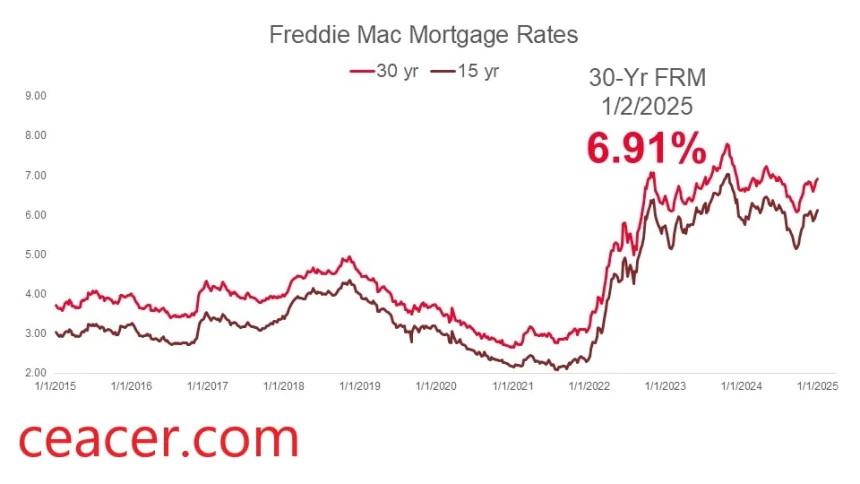

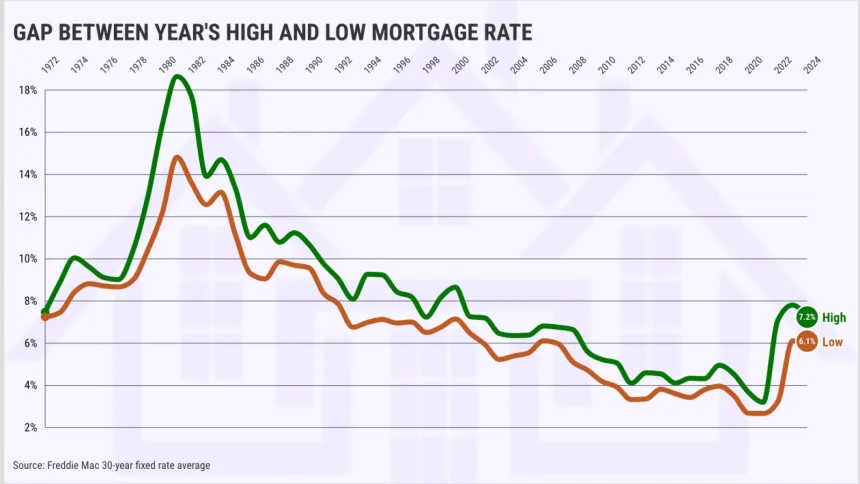

Mortgage rates have become one of the most closely watched numbers in the American economy. For years, they drifted down to historic lows, tempting buyers into the market and fueling a surge in home prices. Then came a rapid climb that left many borrowers stunned, reconsidering their budgets and postponing their home search. Today, mortgage rates move with a kind of restless energy, responding instantly to inflation data, financial policy updates, and a housing market still trying to find its balance.

Understanding where mortgage rates stand now—and why they behave the way they do—has never been more important. Whether you’re buying your first home, upgrading, downsizing, or considering a refinance, the rate you lock in will shape your financial life for years.

This guide explores what’s influencing today’s mortgage environment, how lenders make decisions, and what borrowers can do to secure favorable terms in a market that changes by the day.

Why Mortgage Rates Move the Way They Do

Mortgage rates rarely sit still. They shift based on a mix of economic forces, many of which have little to do with the housing market itself. When inflation rises, investors start demanding higher yields. When bond markets react to new economic data, mortgage rates usually follow. And when the Federal Reserve signals a shift in policy—even before it acts—lenders adjust pricing to match new expectations.

Several factors consistently shape mortgage rates:

Inflation trends.

Inflation plays the starring role in rate movement. When inflation cools, rates tend to ease. When it heats back up, borrowing becomes more expensive as lenders protect their profit margins.

Federal Reserve policy signals.

The Fed doesn’t directly set mortgage rates, but its decisions affect borrowing costs across the financial system. Even a subtle shift in tone from the Fed can move rates within hours.

The 10-year Treasury yield.

Mortgage rates often track the 10-year Treasury bond yield because both appeal to the same type of investor. When Treasury yields rise, mortgage rates typically follow.

Investor demand for mortgage-backed securities.

If investors feel uncertain, they price in more risk, forcing mortgage rates upward. When confidence returns, rates may ease down.

The interplay between these forces creates a rate environment that feels unpredictable, especially for buyers trying to time their purchase.

Fixed or Adjustable: Which Option Fits Today’s Rate Climate?

Choosing between a fixed-rate mortgage and an adjustable-rate mortgage (ARM) is one of the biggest decisions borrowers face.

A fixed-rate mortgage offers stability. The rate you sign for stays with you for the life of the loan, providing predictable monthly payments. In uncertain economic cycles, this steady structure feels like a financial anchor.

An adjustable-rate mortgage (ARM) starts lower but can change over time. The introductory period might look attractive, especially when fixed mortgage rates are elevated. For people who expect to move or refinance, ARMs offer flexibility—but the future adjustments can be unpredictable.

In today’s environment, where mortgage rates shift based on every new economic report, borrowers tend to weigh stability more heavily than they did a few years ago. Still, the right choice depends on your timeline, long-term plans, and willingness to manage rate fluctuations.

Why Different Borrowers Receive Different Mortgage Rates

One of the most confusing realities of the mortgage market is that the “advertised rate” is rarely the rate a borrower actually receives. Lenders adjust their offers based on risk, and each borrower carries a different risk profile.

The biggest factors include:

Credit score.

A strong credit score can shave a meaningful amount off your interest rate. A lower score signals higher risk, so lenders compensate by raising rates.

Debt-to-income ratio (DTI).

Lenders want to see manageable monthly obligations. The lower your DTI, the safer your profile appears.

Down payment amount.

Higher down payments reduce lender exposure and can unlock better rate options.

Loan type and property type.

Primary residences usually qualify for better rates than investment properties or vacation homes.

Even two borrowers with identical income levels can receive different mortgage rates if their credit history or loan structure differs. The key is recognizing that you have more control over your rate than you might think—and preparing accordingly.

How to Compare Mortgage Rates Without Getting Misled

Comparing mortgage rates can feel overwhelming, especially when every lender claims to offer the best deal. But the headline rate is only half the story.

APR, or Annual Percentage Rate, includes interest plus fees. While it isn’t perfect, it gives a clearer view of the total borrowing cost. A rate that looks low on paper may come with higher fees that make it more expensive in the long run.

Borrowers should also compare offers from different types of lenders:

• Traditional banks

• Online mortgage lenders

• Credit unions

• Independent mortgage brokers

Each source uses its own pricing model. Shopping around can produce surprisingly wide differences in mortgage rates, even on the same day with the same borrower profile.

The rate-lock period also deserves attention. Locking your rate can protect you from sudden market swings. In a volatile environment, locking early can save more than borrowers realize.

Is Today a Good Time to Apply for a Mortgage?

Trying to perfectly time mortgage rates is a tempting game—but one that rarely works out. Rates move based on economic news that nobody can predict with perfect accuracy. Instead of chasing the ideal moment, focus on your readiness.

If your job is stable, your credit score is strong, and your housing needs are clear, waiting for a perfect rate environment may cost you more in the long run. Housing prices, competition, and personal circumstances matter just as much as the daily mortgage charts.

A solid mortgage strategy isn’t about guessing the next rate move. It’s about making sure your financial profile is strong enough to qualify for the best pricing available to you at the time you apply.

Why Understanding Mortgage Rates Matters More Than Predicting Them

Forecasts about mortgage rates fill news headlines, but long-term predictions rarely match reality. What borrowers can control—credit score, debt levels, savings, lender choice—matters much more.

A borrower who understands how mortgage rates work can navigate the market with confidence. They can decide when to lock a rate, when to negotiate lender fees, when to refinance, and when to adjust their budget.

Knowledge isn’t just power; it’s money saved over the life of the loan.

Final Thoughts: A Clear Approach in a Shifting Market

Mortgage rates today sit at the center of financial conversations, shaping the decisions of buyers, sellers, investors, and refinancers. The landscape may feel unpredictable, but borrowers are not powerless. By understanding how rates move, comparing lenders carefully, and strengthening your financial profile, you can secure a mortgage that supports your long-term goals rather than complicates them.

The housing market changes quickly, but a well-prepared borrower can move through it with clarity and confidence.

Share

What was your reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0